Since Harry Markowitz developed modern portfolio theory’s mean-variance optimization (MVO), financial advisors and wealth managers have been confronted with a crucial question: What is the relative importance of risk tolerance (the investor’s attitude toward risk) compared to risk capacity (the investor’s ability to endure negative outcomes)?

I must confess that I have been perplexed by this question for decades. My frequent co-author, Paul Kaplan, and I believe we have solved this 50+ year conundrum using an expanded MVO optimization model called net worth optimization (NWO).

I plan to discuss our findings on my panel at CFA Institute LIVE 2025 in Chicago in May.

How did we get here?

The goal (objective function) of mean-variance optimization is to maximize the expected return of a portfolio, minus a personalized penalty for the expected risk (variance) of the portfolio. Personalized penalty is the investor’s risk tolerance coefficient multiplied by the variance of the portfolio.

In MVO, the “risk tolerance” coefficient is a single number reflecting the rate at which the investor is willing to trade off more risk in pursuit of more expected return. Knowing the investor’s risk tolerance coefficient allows you to solve for the corresponding MVO efficient portfolio.

In the economics literature and the works of Nobel Prize winners like Paul Samuelson, risk tolerance is clearly related to the investor’s attitude toward risk, not risk capacity.

Advisors frequently have a deep understanding of their clients’ situations. This might include information on additional accounts, spousal assets, compensation information, mortgage payments, etc. Some clients may be very comfortable with risk, but with little capacity for adverse outcomes given their circumstances. While other clients are extremely uncomfortable with risk but can tolerate adverse outcomes with little impact on their financial well-being. Advisors find themselves navigating what has been a highly subjective risk tolerance (attitude) versus risk capacity conundrum.

Two Approaches to Risk Capacity

Pragmatically, there have been two approaches that explicitly focus on risk capacity.

The first approach is a common feature of the “scoring” component of risk tolerance questionnaires. When scoring the responses to a risk tolerance questionnaire, there are frequently two scores: a risk tolerance score and a time horizon score. The time horizon score serves as a crude proxy for the investor’s capacity to take on risk that limits which portfolios are deemed suitable.

The second approach is probably less known to practitioners but prevalent in the practitioner-oriented literature. This approach is best represented by the “discretionary wealth hypothesis” primarily put forth by Jarrod Willcox.[1] In these types of approaches, the investor’s attitude toward risk is discounted or ignored, and financial ratios like the ratio of assets-to-liabilities are used as the primary factor to estimate a so-called “risk tolerance coefficient. I use quotes to distinguish this from the economic definition of risk tolerance as an attitude.

Net Worth Optimization (NWO)

In our 2024 CFA Institute Research Foundation book, “Lifetime Financial Advice,” Kaplan and I put forth NWO. It is a significant extension of MVO. NWO includes all of the investor’s assets and labilities in the optimization, especially human capital, and it optimizes the investor’s holistic economic balance sheet.

An investor’s economic balance sheet includes all his or her assets — home, land, collectables, and all financial assets. Most importantly, the economic balance sheet includes the capitalized value of the investor’s lifetime of earnings — human capital. For many people, the mortality weighted net present value of all future labor income, including deferred labor income in the form of defined benefits and social security, is their single largest asset.

The lifetime of cash flows stemming from human capital is frequently reminiscent of the cash flows you would receive from a large, inflation-linked, long-duration bond. Others have less steady human capital that might resemble a stock/bond mix.

On the right-side of an economic balance sheet, we all have ongoing expenses, such as rent, a mortgage, insurance, medical costs, and food. While these may not be legal liabilities, these expenses are often inescapable. Collectively, their capitalized values form what we think of as the investor’s nondiscretionary consumption liability.

Just as a balance sheet is an important indicator of a corporation’s financial health, a holistic individual economic balance sheet is an excellent indicator of the investor’s overall financial health and capacity for taking on risk. The difference between the total value of all assets and all liabilities is net worth. Hence the term net worth optimization or NWO.

NWO includes all the major economic balance sheet entries. Nontradable entries — the investor’s human capital and nondiscretionary consumption liability — are included in the optimization, although the optimizer cannot change the net present value of either. These nontradeable assets are modeled as portfolios of asset classes, which enable us to derive proper market-based discount rates and understand how they interact with the rest of the balance sheet.

Imagine a 45-year old pharmaceutical scientist with a base salary of $200,000, adjusted each year for inflation, who receives $100,000 nominal restricted stock units with a five-year vesting schedule who also expects to receive approximately $25,000 per year from social security starting at age 65. One could model this person’s human capital as nearly 2/3rds long-duration-inflation-adjusted corporate bonds with a duration corresponding to the 20 years of cash flows, and nearly 1/3rd mid-cap stocks (reflecting the size of the company).

You could refine the 1/3rd mid-cap stocks by modeling them based on the pharmaceutical sector or even using the specific stock in question. The current net present value of social security isn’t worth that much today, but it too should be accounted for properly. The expected returns on each form the basis for a weighted average cost of capital for calculating the value of the scientist’s human capital.

The capitalized value of the investor’s nondiscretionary consumption liability, which is somewhat like issuing a long-duration-inflation-linked bond with outgoing coupon payments, is included as a nontradable negative holding in the optimization.

Then in the presence of nontradable assets and liabilities NWO determines the optimal asset allocation for the investor’s tradable assets — an optimization that fully accounts for the investor’s ability to take on risk.

Moving through time life happens. The client could be fired, the value of stock could go up/down, inflation could increase/decrease, start a family, or an uninsured home on the coast could be washed away, etc. Critically, as the value of the person’s assets relative to the value of liabilities evolves, the person’s financial health and ability to take on risk evolve. Unlike asset-only MVO, NWO fully captures the investor’s ability to take on risk.

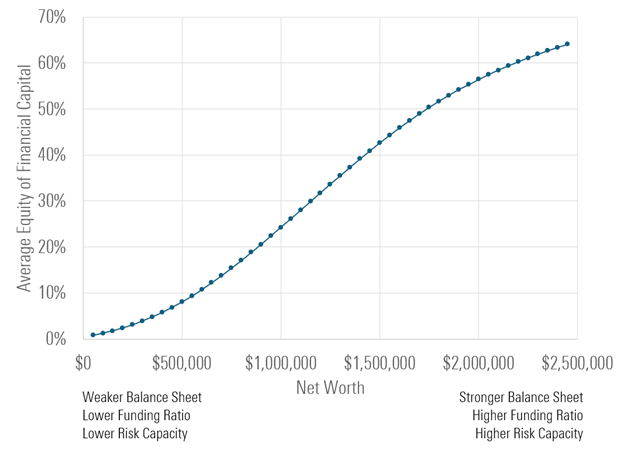

In a February 2025 Financial Planning Review article, “Net Worth Optimization,” Kaplan and I discuss more than 8,000 net worth optimizations in which we varied the investor’s human capital and the composition of the investor’s economic balance sheet. As Figure 1 shows, after controlling for the investor’s risk tolerance, the amount of equity exposure for tradable financial assets increased with the relative strength of the investor’s economic balance sheet. We believe this is a new, but intuitive result.

Figure 1: Optimal Financial Capital Equity Level.

Source: Idzorek and Kaplan (2025).

In Figure 1, each dot is the average equity level of financial capital from 180 net worth optimizations corresponding to different combinations of human capital and risk tolerance. As the holistic economic balance sheet strengthens, all else equal, it is optimal to take on more risk.

Conundrum Solved

With NWO there is no conundrum. We no longer need to ask which is more important, the client’s attitude toward risk or the client’s capacity to take on risk.

NWO allows you to use the client’s risk tolerance as it was intended — to reflect the client’s attitude toward risk. Most importantly, NWO simultaneously goes well beyond the time horizon proxy of risk capacity by fully reflecting the client’s ability to take on risk as captured by a holistic and evolving economic balance sheet.

With the advancement of net worth optimization, the financial planning industry should move from MVO to NWO.

References

Idzorek, Thomas M., and Paul D. Kaplan. 2024. Lifetime Financial Advice: A Personalized Optimal Multi-Level Approach. Charlottesville, VA: Research Foundation of CFA Institute. https://rpc.cfainstitute.org/sites/default/files/-/media/documents/article/rf-brief/lifetime-financial-advice.pdf

Idzorek, Thomas M., and Paul D. Kaplan. 2025. “Net Worth Optimization.” Financial Planning Review 8 (1): e1200. https://onlinelibrary.wiley.com/doi/epdf/10.1002/cfp2.1200

Straehl, Philip U., Robert ten Brincke, and Carlos Gutierrez Mangas. 2024. “Should Your Stock Portfolio Consider Your Career?” Morningstar Research Paper, June 21.

Wilcox, Jarrod W. 2003. “Harry Markowitz and the Discretionary Wealth Hypothesis.” Journal of Portfolio Management 29 (3): 58 – 65. DOI: 10.3905/jpm.2003.319884

Wilcox, Jarrod W., and Frank J. Fabozzi. 2009. “A Discretionary Wealth Approach for Investment Policy.” Journal of Portfolio Management 36 (1): 46-59. DOI: 10.3905/JPM.2009.36.1.046

Wilcox, Jarrod W., Jeffrey E. Horvitz, and Dan DiBartolomeo. 2006. Investment Management for Taxable Private Investors. Charlottesville, VA: Research Foundation of CFA Institute.

[1] Examples include Wilcox (2003), Wilcox, Horvitz, and di Bartolomeo (2006), and Wilcox and Fabozzi (2009).