Ethereum’s active addresses have declined sharply since the beginning of the year, dropping from around 525K to approximately 333K. This decline has coincided with a weakening price trend, stabilizing near $1.8K at press time.

The sustained decrease in activity highlights a notable reduction in user engagement and transactional volume across the network.

Source: CryptoQuant

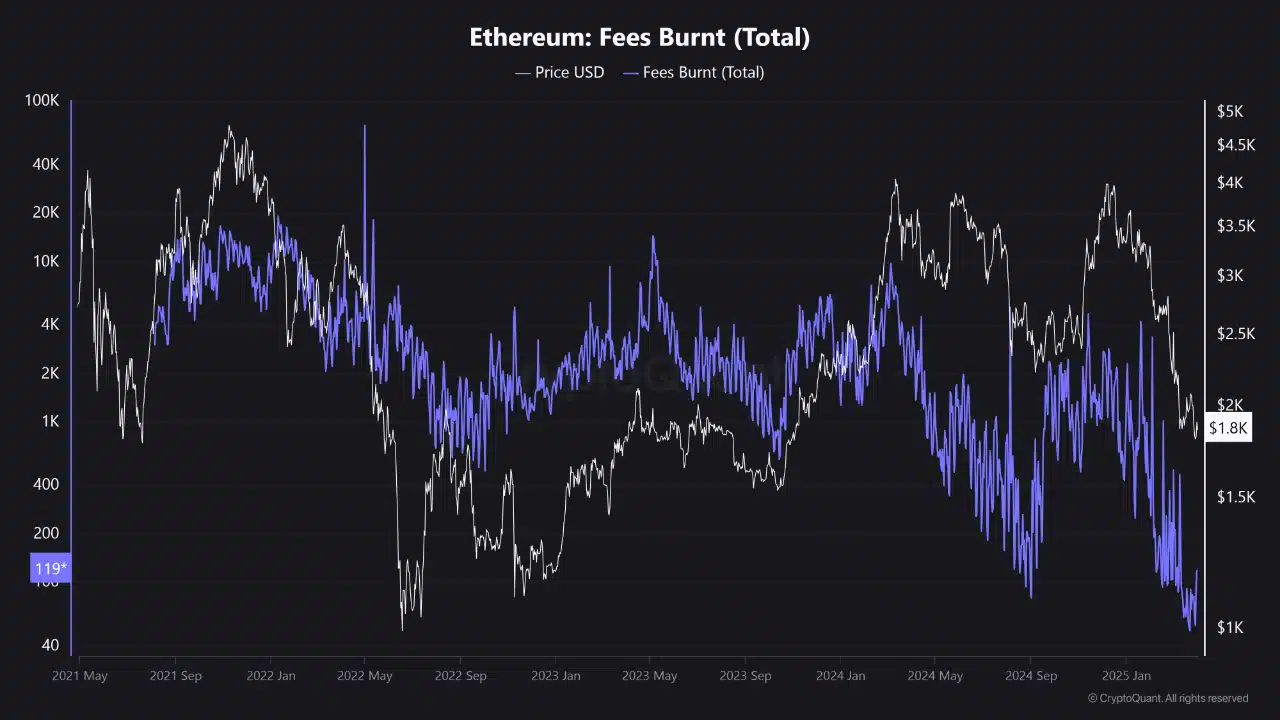

Recent data also reveals a sharp reduction in Ethereum’s total fees burnt, echoing the downtrend in active addresses and suggesting reduced on-chain activity.

Lower burn rates could indicate less network congestion or fewer high-priority transactions, reinforcing decreased usage and network momentum.

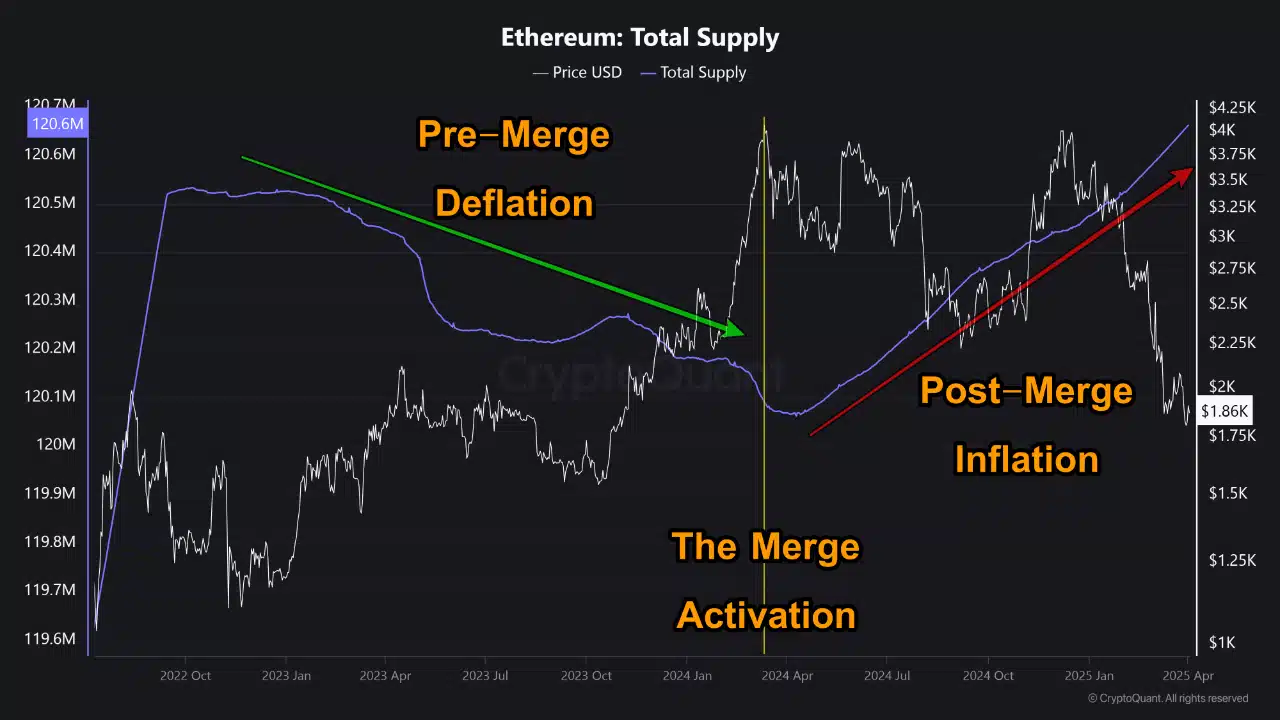

Inflation by design?

Ethereum’s Dencun upgrade was heralded as a step toward long-term network sustainability. However, the upgrade’s aftermath has sparked debates, as Ethereum’s total supply has surged.

The data highlights a stark contrast between the pre-Merge deflationary period — marked by a declining supply — and the post-Merge inflationary trend.

Source: CryptoQuant

The Merge initially brought optimism with its deflationary benefits, reducing Ethereum’s issuance rate and burning more tokens than were created.

However, after the Dencun upgrade, the burn mechanism has struggled to counter inflation due to declining transaction volumes and lower network activity. With fewer fees being burned, the network has returned to inflationary territory.

Although the upgrade aimed to strengthen Ethereum’s resilience, it unintentionally exacerbated inflation during a period of reduced on-chain activity.

This shift has made Ethereum’s post-Merge reality appear misaligned with its original deflationary vision, raising doubts about the long-term effectiveness of the burn mechanism.

It remains uncertain if future updates, such as the Pectra upgrade planned for the 30th of April, can achieve a better balance between sustainability and inflation control.