The rapid rise of the Taiwan dollar in Q2 has fueled speculation of a modern-day Plaza Accord 2.0 — a possible coordinated intervention to weaken the US dollar, similar to the original 1985 Plaza Accord. That historic agreement, signed by G5 nations, aimed to reduce the US trade deficit through a managed dollar depreciation. But today’s global economy is far more complex, and analysts caution that repeating such an initiative could trigger unintended consequences.

📉 FX Volatility Risks for Taiwan and Global Insurers

A major concern involves the impact of a weaker US dollar on Taiwanese life insurance companies, which collectively hold assets equivalent to 140% of Taiwan’s GDP, much of it in USD-denominated bonds. These holdings are only partially hedged, exposing firms to large currency mismatches. A sharp decline in the dollar would reduce the value of these assets while the liabilities remain in Taiwan dollars, creating solvency pressures.

Additionally, these insurers are heavily exposed to duration risk, holding long-maturity US bonds. A selloff in these assets would raise long-term US interest rates and could propagate interest rate volatility globally.

🌍 Broader Global Impacts: Carry Trades and Liquidity Flows

Taiwan isn’t alone. Japanese carry trades — selling yen to buy US assets — led to market disruptions in late 2024. A synchronized dollar depreciation could lead to capital unwinding, further destabilizing markets and raising borrowing costs.

Moreover, the US relies heavily on foreign reinvestment of trade surpluses into US Treasuries. A weaker dollar and lower US trade deficit could reduce this inflow, undermining Treasury market liquidity and complicating debt financing.

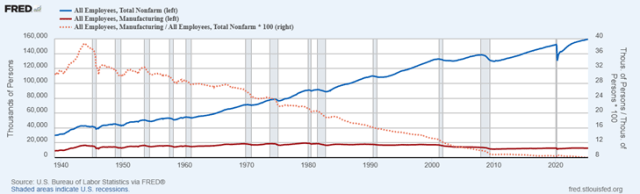

🏭 US Manufacturing: Leaner, Smaller, Slower to Benefit

The original Plaza Accord helped stimulate a then-robust US manufacturing sector. Today, however, manufacturing accounts for just 9.9% of GDP (vs. 18.5% in 1985) and 8% of non-farm payrolls. With fewer jobs and stagnating productivity gains, the sector’s ability to benefit from currency shifts is more muted.

According to past studies, exchange rate changes influence trade balances with a two-year lag. That means any benefits to US exports could take years to materialize — a long wait in an environment of heightened fiscal risk and debt sensitivity.

⚠️ Cost-Benefit of “Plaza Accord 2.0” in 2025

A modern Plaza-style agreement could pose more risks than rewards:

-

⚠️ Increased FX volatility and asset-liability mismatches for global insurers

-

⚠️ Reduced foreign demand for Treasuries amid a shrinking trade surplus

-

⚠️ Minimal manufacturing employment gains due to structural changes

-

⚠️ Potential destabilization of capital markets

💡 Conclusion: Currency Coordination Isn’t What It Used to Be

Calls for a “Plaza Accord 2.0” underscore the growing pressure to fix trade imbalances and boost US industry, but the global economy today is far more interconnected and fragile than in 1985. Any coordinated depreciation of the US dollar could ripple across debt markets, insurance portfolios, and monetary policy.

Policymakers must weigh these systemic risks against potential gains for a smaller, leaner US manufacturing sector. In 2025, the risk-reward calculus for global currency coordination is more complicated than ever before.